Top 10 Ways To Cut Down Your Spending

Because who couldn't use a little extra cash

We are all at different points in our financial journey. For most of us, when just starting out, money is tight. If you happened to navigate the flurry of bad career and college advice - just follow your passion and go to your dream school - and you actually landed a good paying career right out of college, you are way ahead of the game.

You have capital and you have free time and that is a potent combo for growing your career & side business. If you have a safety net in place, you can take more risks and reap the rewards. Bull and many rich Gs have this path covered.

For those of you whose passion was writing fan-fic of big-haired 80s cartoon characters finding love in surprising places and went to a $70k a year small university with more amenities than successful graduates…money is tight…tighter than Rogue and Optimus Prime’s hopelessly trying love in a world that doesn’t accept giant transforming trucks and mutant relationships…

Or maybe you do have a good paying job and should be getting ahead, but every month it feels like you are treading water.

Whatever the case, if you think there may be some areas to cut expenses in your spending, this is the post for you.

Why Cut Spending?

I’ll be the first to say that budgeting is not something that I find fun.

It is why I recommend automating savings right off the top and automating increasing it every year. If you save 25% of your income when you start working and increase it every year by 1%, you will be saving over half your pay by 50. Do that and how you shuffle around your spending doesn’t matter.

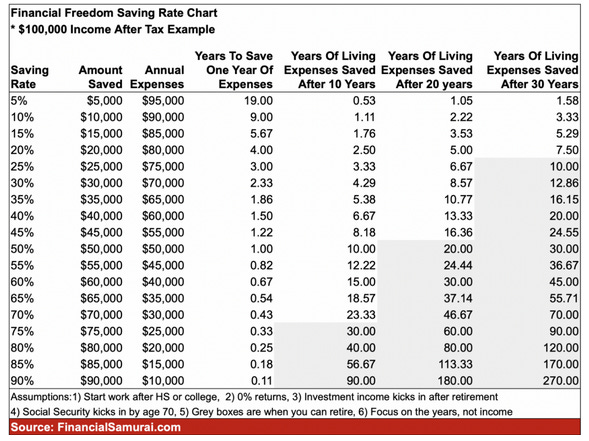

I’m not going to recreate the below table, but there are dozens of these floating around the FIRE-verse. I have my issues with FIRE and with this analysis, but it gets the point across. Saving 25-50% over 25 years and you are in a really strong financial spot.

This is because you are both 1) Saving & investing a lot of your income, and 2) Controlling lifestyle creep by increasing your savings & investing over time.

Cutting your expenses in a reasonable and low time-sunk kind of way can be powerful for anyone not independently wealthy.

But once you remove the big easy items, you need to move on to making more money. If you continue to try to cut more and more, you end up in a game of diminishing returns. Making a phone call to save $100 a month is worth it. Cutting coupons and driving to 4 grocery stores taking a full day a week to save $20 a week not so much.

Every item on this list is here because it is either:

A large expense save or

A small expense save that doesn’t take much time to do

Save a couple grand a year, incorporate a few money-saving habits, and minimize your time spent on it. Then move on to find ways to increase your earnings.

Every year or few revisit this list as a lot of these items creep back in.

If you incorporate all these items, you can free up $1,000s a year that can help your finances.