So You Won The Lotto...

...Yes We constantly say don't waste mental space dreaming about it...But here it is

“ThE LoTto iS a sTupId Tax”

It isn’t. We already addressed this midwit, oft-repeated nonsense. Lotto is the most asymmetric bet you can make. The ‘tax’ on lotto is people spending more than a few $ per draw and daydreaming of lotto wins instead of building.

But Twitter is full of bad advice to lotto winners. A few well known personal finance bloggers had tweet threads with a mix of demonstrably false & outright wrong pieces of advice. A sampling:

Claim it anonymous - great in theory, in practice only 6 states allow anonymous lotto claiming (Delaware, Kansas, Maryland, North Dakota, Texas, South Carolina). A handful of others let you set up an LLC to claim it.

Drive to a state you can claim it anon - Nope, you need to claim the ticket in the state you purchased it. But at least this guy knew / did miniscule amount of research to know some states don’t allow anonymous claiming, but didn’t go far enough to read the rules of the actual lotto

Drive to a low tax state to claim it - Nope, see above

Sign your ticket right away - Nope, now you just lost the chance to put it in an LLC or Trust since it is in your name

Put the $1.9 Billion in dividend paying ETF to live off ‘passive income’ - did you just tell people to take the lump sum and put it all in a single asset type?

So you won the lotto, what do you do?

Get Professionals

Don’t sign the ticket!!!!

Take a picture of yourself with the winning ticket. Make copies of it. Put them in a safe. Immediately contact professionals. At a minimum you want:

Tax lawyer who specializes in dealing with ultra high net worth (UHNW) clients

Family law & estate planning lawyer who specializes in trusts & estate planning

Certified public accountant (CPA) who deals with UHNW clients

Financial advisor (not any schmo giving advice, an actual advisor who is a fiduciary. That is a key distinction as fiduciary is the higher standard of putting your needs first).

You just won the lotto, don’t be cheap. You need a team to set you up. You are in the big leagues now, so having all 4 of the above in the same meeting to work together is key.

And don’t feel like you need to go with the first person that comes up in a google search. You are the prize here.

Interview them.

Make sure you vibe.

Make sure they will tell you no. What is the point of a team if they agree with everything you say, including investing heavy in that fanfic of the team up of big haired 90s cartoon ladies

Wait

This is probably the hardest part, but wait. Like don’t do anything.

You have a plan from talking to the professionals. You have ample proof you won and have the winning ticket. Unless you bought your ticket in one of the 6 states that allow you to claim it anon, put it in a safe for a while. You don’t want to claim it while the media is in a frenzy. Wait.

Trying to claim it once the hype dies down isn’t the only reason to wait.

Your in shock. You went from low to modestly wealthy to elite over night. You are prime to make dumb decisions. Let it sink in for a few days.

People know you. If you walk in and take a huge steaming shit on your bosses desk, open mouth kiss Vanessa that cute girl in HR, and flip everyone off while kicking over garbage cans the morning after a big lotto is won…people will put 2 and 2 together. Carry on with life (or if you really hate your job take pto, but honestly show up and scroll your phone for 8 hrs.)

Really cement your post claiming plans so you don’t screw it up.

What Protective Steps Can You Take While You Wait?

While you are waiting, you shouldn’t be doing nothing. What pre-emptive moves can you make to protect yourself?

Many towns have home ownership publicly available. Most people don’t set up an LLC to buy their personal home. Can you do anything to make it harder to find you?

Same with your phone number.

While you have professionals see what you can do to insulate yourself from people trying to find you. Hire a personal security guy to advise you if you have to.

When your name goes public, people are going to try to find you with their hands out or worse, to rob you.

Saying NO is going to be your go to for a while. But most of us are good people, and if 100s of people can access you with their hands out and sob stories. The harder it is to locate you the better.

We are security experts, so probably a lot of stuff we are missing here. But the point is, find out what you can do to protect yourself from beggars, robbers, and grifters.

Claiming Your Prize

Ok. Time to claim your prize. But first, what are the rules in your state for claiming the prize?

Do you have to do it in person?

Any rules against wearing a mask?

Any rules against fake glasses and beard? Wig?

What if you have a “credible” concern for your life? Maybe…I don’t know…an ex or old associate has been “making threats”? What is the burden of proof?

What is the minimum threshold of the name you need to provide? Nick names? Maybe you suddenly decide to revert back to that “nickname” that everyone definitely calls you by?

Its 2022, have you been a Bob your whole life, but this lotto win made you feel like a Becky? Wig, comical make-up, big glasses, kind of Becky?

You get the point. Just because you can’t be anonymous doesn’t mean you can’t do everything in your power to hide your identity.

After Claiming

Go somewhere.

Get a hotel under a different name in your local area if you have to. But if people can track you down at your home address they will.

Take time.

Now here is the next place people screw up. Take the annuity. Mega jackpot lottos default to annuity payments for 20 to 30 years usually. It is an increasing annuity, meaning each payment will be larger than the last, about 5% larger.

Just take the annuity. For the $1.9 Billion lotto, the annuity started at ~$29 million. Your last payment would be over $115 million.

“But F’er…what about time value of money?”

Thanks for reading…but also throw every rule out the window.

You are going to get paid 8-figures a year for the next 30 years. The name of the game is not fukting it up.

Even assuming 50% taxes, you have almost $15 million in year 1 to spend. Let’s assume your a smooth brain and blow through it all. Well here comes almost $16 million in after-tax money in year 2. You really are bad at this and who doesn’t need a fleet of lambos and you waste it all. Year 3 is $17 million more….you get the point.

“I’m responsible and will buy a vanguard fund with the ~$700 million (after-tax) lump sum”…then the market drops 50%….

And then you need to pay more taxes…wait more taxes? Yup keep reading to find out how you just screwed up without knowing

But the annuity…You get 30 chances to mess up.

We repeat….you made it…you are set for life. 8 figures a year in after-tax cashflow.…you don’t need to go risk on. Your goal is to not blow up.

How Lotto Winners End Up Broke, AKA TAKE THE ANNUITY

Sometimes, the best way to learn what to do is to see how others screwed up so you learn what NOT to do. (Or said another way as one of our favorite quotes…

“Invert, Always Invert”

So how do lotto winners end up broke?

They 100% take a lump sum

They don’t gather a competent team

They start buying liabilities for themselves & others

They don’t understand taxes

Let’s start at the back and work our way to the front.

Taxes on Lotto

You won the lotto. You elected the lump sum cash payout of ~$920 million instead of the annuity for $1.9 Billion. The IRS takes its taxes out for ~$220 million and your after tax money is ~$700 million.

Then April 15th comes around and you get hit with another $112 million in taxes.

You are confused. Didn’t the IRS already take $220 million?

Well, the way withholdings work is only 24% of your lotto winning is withheld. You true up the rest at tax time. This makes sense with smaller winnings and marginal tax rates where your effective tax rate isn’t the top rate.

If you win $1 million and that is your total income, your effective tax rate is only 30%. Many lottos are $100,000s meaning your effective tax rate will be sub 24%.

But clearly if you lump sum $700 million in a single year, your effective tax rate is 36.999%. But rules are rules so ‘only’ 24% gets withheld up front.

Go back to our earlier example. You take the $700 million post 24% withholding and put it all in a low-cost Vanguard fund. Market drops 50%, and now you need to withdraw $112 million of your $350 million remaining balance to pay the tax bill. Ouch.

And now you look at state & local taxes which can be 0-13% (Hey NYC at 13%). So you love the Big Apple for the city life? You are paying another $120 million in taxes on your winnings. Here is a list of every state taxes and a calculator tool if you want.

$700 million drops to $350 million due to bad investments/timing, minus $112 million remaining federal tax, minus $120 million in state and local tax = $118 million left.

Sure we took it to an extreme to make a point. But you won $2B and are now sitting on $120 million. You have 6% of your advertised winnings before you even spent a dime.

Buying Liabilities For You & The Boys

Still, $120 million is enough to live lavish. You buy the big mansion and some houses for your people. A few fancy cars. A modest yacht. You are living the good life…Its not like you got a private jet (please tell us you didn’t buy a jet).

Well, all of those items come with ongoing costs. And all you have is your lump sum lotto earnings to live off for income. How much ongoing cost is your $10mm mansion, $1mm cars and $5 million yacht?

State Property tax: $28k to $250k a year depending on where you live

Homeowner insurance: 5-figures a year

Local auto taxes another 1% per year

Tax on Yacht another 1%

Maintenance costs are a lot

Let’s just round it to $2 million a year in maintenance and taxes on a few luxury items. And this doesn’t include the cost of all the finer things in life like landscaping, decorating the big house, vacations, etc etc.

This issue isn’t spending, so much as lack of cashflow.

You didn’t slowly work up to that level of wealth and you didn’t get there with a business or work or anything replicable.

And instead of preserving your principle and living off the dividends/interest, you are slowly eroding principle.

With NO new money coming in.

This high level of fixed costs is what ends up bankrupting lotto winners. And since the lump sum is so much less after-tax than the headline number, people spend it all. Or their investments don’t work out because of bad timing.

Bad Advisors

Most lotto winners skip the step of building a good strong team to guide them. “Its so much money” and “I was living on less” is the logic that drives them.

And people make poor decisions.

We repeat, most lotto winners aren’t successful business owners. They tend to be lower to middle class.

So when that great pitch comes in to invest in start-ups, real estate, private investment opportunities, etc, there is little in the way of being able to discern if it is a good investment.

[Side note - one of the grandparents in our family had a fairly large windfall from an inheritance from a relative. They refused guidance and put it all into oil well drillings. It was a ‘sure thing’ as almost all the wells hit oil in the area. As you can guess, the half dozen wells they purchased were all dry. A fortune was lost.]

Having no or poor advisors to ‘save money’ is a huge oversight.

Taking The Lump Sum Over The Annuity

(Do you see a theme?)

Terrible advice.

Sure on paper having $929 million seems like a no brainer (when its actually $700 million after withholding tax #1, and $588 million after April 15th tax day, and if you are in a high-tax area like NYC another $120 million in state and local tax for $468 million).

But that is 1 chance. You blow it you are broke. There is no more money coming in.

“But My gooroo says to buy Vanguard Dividend at 3% divi and live off that money. Sounds reasonable. Let’s say post all taxes you lump sum is $500mm to invest in vanguard. 3% divi on $500mm is…. $15 million pre-tax.

So you take the lump sum. Take massive bullet investment risk. Take a huge tax hit. Run the risk of losing it all. And your end game is to invest it to turn it into a stream of $15mm pre-tax cash flow.

A stream of cash flows has a name…it’s escaping me…o yea. An annuity. But one that pays $15mm a year instead of one paying $30mm in year 1 and increasing each year after.

Yes. Our “peers” in the space who are giving advice on finance, fail to get to this very basic conclusion.

Allright, You’re Convinced. What Do You Do With The Annuity?

[Note - this is illustrative. It is the spirit of what we would do, but not an exact blueprint.]

First, choose a spending target. Something like 1/3 of your annuity is probably a decent rule of thumb. For this mega winner, with an annuity starting at ~$15 million after a 50% tax rate, lets just say $5mm spending with a 3% adjustment each year.

Year 1 you can spend $5mm of your payout and in year 30 you have a spending budget under $12 million.

The rest you invest.

What do you invest in? We would say a nice barbell strategy where you start with a high allocation to low-risk investment and a small allocation to higher risk stuff. Over time as you build up an ‘unspendable’ income stream from your low-risk stuff, you invest more and more into the high risk.

For simplicity we will choose 4 asset classes in order of riskiness

CD Ladder & Savings accounts

Short-term Muni bonds

Equity

Crypto

We might do something like the below where:

Safest: CDs start at 90% and decrease allocation by 5% per year

Safe: ST Munis at 5% per year

Risky: Equity is remaining allocation

Riskiest: Crypto starts at 2% and increases 2% per year to max 40%

This way you are securing a large, ‘safe’ bucket of cashflowing assets (CDs & ST Munis) up front.

[Note - FDIC insures money in each bank up to $250k. SIPC covers $500k in investment accounts and $250k of that can be cash/cash equivalents. You will need a lot of banks to do the CD ladder in $100 million balance. Just hire someone to watch your bank accounts.]

Then adding on more risk and growth potential later with Equity & crypto.

[F’er Note - short-term munis are basically local state and town municipal bonds with 2 years or less to maturity. These tend to yield a bit more than a bank account, but with less than 2 year to maturity, there is little risk of default. Munis also tend to be tax-advantaged.]

Remember, you are already spending $5mm a year from your annuity payout and that is growing at 3%. So any investment cashflow you can just reinvest back into investments for 30 years since you aren’t touching the principle.

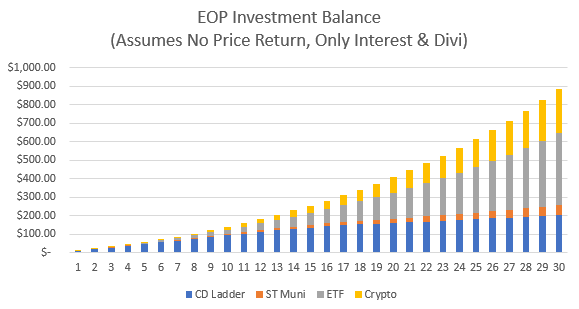

If you assume no growth in prices of your equity and crypto and CDs give you 3% yield, munis 4% yield, and ETFs 2% dividend, your portfolio looks something like this:

30 years later you have almost $900 million invested even with 0% growth in ETFs and crypto. And you are cashflowing ~$12.5 million a year after-tax.

Sure, this is simplistic as you probably can open your investment world up to more than just 4 assets. But you get the idea. You have spent $238 million over the 30 years and still have at a minimum, $900 million in assets and enough cashflow to live off.

[Note- We would probably buy some permanent life insurance in there as well to move money to trusts for kids and grand kids to keep it private and have control on when they get the money.]

Now you tell me, why are you taking a lump sum and a ton of investment risk?

“I want the money if I die” is one other reason said on Twitter for the lump sum. Well, if you die, your estate gets the remaining CF. Per the lotto site:

“If a jackpot winner dies before receiving all annual installments, the balance of the prize will be paid to the winner's estate. Upon receipt of a court order, annual prize payments will continue to be paid to the winner's heirs. Other provisions may also apply depending on the laws of the lottery paying the prize.”

Conclusion:

This free post is a bit of mental masturbation. The likelihood of any of the thousands of people subscribing actually winning lotto is immaterial (but if any of you do, we will help advise your finances).

But it is a fun one to write.

The answer is so absurdly clear to us on what to do, the fact there are so many bad takes out there is mind bottling.

If you win lotto. Be Anon as possible. Get a good team to advise you. Take the annuity so you can’t go broke. And secure safe cashflows first.

And stop taking advice from finance gooroos who repeat the same 2 talking points no matter what (“BuY VoO”).

Even smaller jackpots (Powerball minimum jackpot is $40 million, so low $20mm lump sum and ~$10-12 million post-tax) makes sense to take the increasing annuity. Sure you can’t spend $5mm a year, but all the above logic is still valid.

And this is more time on lotto than you should spend. You should be building your side incomes since that is a much higher probability of success. Thanks for reading, but go build something.

Good luck Anon

These articles really are enjoyable to read, and shows how knowledgeable you are on finances! Thank you for the hard work on it.

I can see the logic behind the annuity strategy. One question for you, though: any concern about a scary future world where the highest income tax brackets get to the point of 60, 70, or 80%? In theory, now might be the lowest taxes are ever going to be looking forward - would it be more tax efficient to tax everything in the lump sum now?