Rewards get all the love. Everyone wants to see the big return or talk about the big payoff on an investment.

Chicks dig the long portfolio.

Managing risk is like the Rodney Dangerfield, it gets no respect. However a little risk management goes a long way. Let’s see if we can put some ReSPeKT on it.

We will cover a few basic risk management areas in this intro post. But don’t worry, risk management is near and dear to our hearts here. There will be plenty more deeper dives into the topic.

There are a lot of different types of risk to be aware of. There is the risk your portfolio goes down, sure, but that isn’t a killer. It gets undue attention because it is very visible. But having a $100 stock go to $50 never bankrupted someone who avoided leverage and had ample liquidity.

Those are the real killers you need to be aware of: Liquidity and Leverage.

Holistic Risk Assessment

“F’er, I don’t use leverage, and only buy ETFs so I am diversified”.

Great…But you are talking about your stock portfolio.

Do you have a mortgage?

Do you have a sufficient emergency funds & multiple income streams?

Do you have other accounts, stock with your employer, etc?

Most people take a myopic view of risks. It is easy to followmental accounting fallacies and look at our investment portfolio in isolation, or check accounts in isolation, or examine our personal lives in isolation.

You need to look at risks holistically.

We have a family friend who is a great example of taking myopic risk assessment. She was a real estate agent. She owned a few rentals. When she invested it was in fundrise (the crowdfunding RE investment). She feels comfortable with real estate. Each choice isn’t bad in itself. But holistically, she is almost entirely concentrated in real estate. If the RE market tanks, her income source, rentals, and stock portfolio can all get crushed simultaneously.

Another example in the corporate world is company stock.

Many companies offer you the ability to buy discounted shares of corporate stock, usually with 10% of your paycheck (when managed right, its free money).

Many companies also have their 401k match automatically purchase shares of company stock.

As you move up the company, you get long-term incentive in shares/options of the company stock that slowly vest over multi-year periods.

Each year, it is very easy to have 10% of your annual salary in stock purchase, 4% of your annual salary in 401k company shares, and 50%+ of your annual salary in long term comp. So ~ 2/3 or more of the total base pay is in company stock.

If the company pays you $100k after-tax, thats $10k in stock purchase, ~$4k in 401k, and $50k in long term comp. Go 2 years and you will have $128k in company stock.

Then your company pulls an Enron - you lose your salary sure, but you lose multiples of your salary in all the company stock you owned. Taking a holistic look, you would notice your only income and a huge amount of your savings are all tied to 1 company.

Some people take it even further. There is a whole industry around having a ‘Plan B’ with 2nd passports, citizenships, etc. (Honestly, if you made it financially already and have enough money, there is no reason not to.)

We are going to focus mostly on our portfolio here, but as we are going through investment specific strategies, don’t forget your portfolio doesn’t exist in isolation.

What are some strategies that are deployed to manage risks?

Barbell Strategy

A barbell strategy is any strategy where you take the 2 available extremes for your investing. The theory is that by bifurcating your portfolio into very low risk & very high risk investments, you will outperform a more moderate portfolio construction. The conservative portion of the portfolio provides stability and liquidity while the aggressive portion provides upside return potential.

For instance, you invest your portfolio in US Treasuries and risky tiny companies. US Treasuries are currently thought of as a near risk-free asset, whereas micro-cap companies are seen as a very high-risk/high-reward project.

Another example is in fixed income if you invest in 3-month maturity bonds and 30-year maturity bonds. That is some of the shortest & longest maturities available. You keep the 3-month allocation for liquidity purposes and the 30-year for locked in higher yield.

The thought around the barbell strategy is the lower-risk side will offset the risk from the higher risk side.

Maybe on your personal finances, you have a bunch of CDs for your emergency fund, and then invest largely in crypto with any excess and avoid more TradFi assets like stocks & bonds completely. If so, you are setting a barbell strategy.

Ladder Strategy

When you take a ladder strategy, you are taking a much more uniform approach to your investment portfolio. A ladder strategy you spread your investments across all the risk-levels.

For example, if you view CDs as very safe and crypto as very risky, you will also allocate some of your investments into stocks & bonds.

If you are investing in fixed inome securities, you will allocate to all maturities.

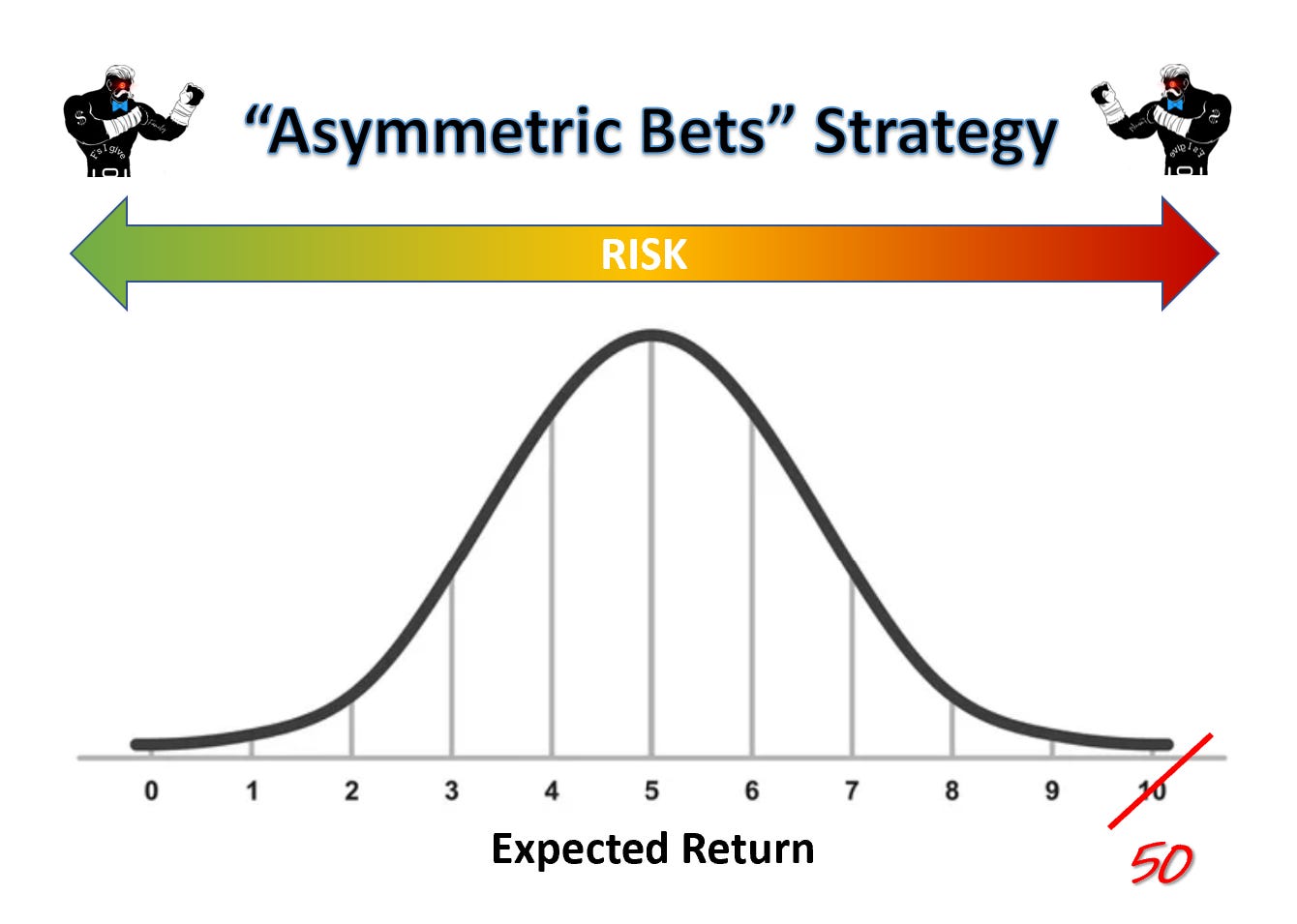

Asymmetric Bets

Making asymmetric bets is the philosophy that the markets do a poor job of pricing tail risks. Because most investors are investing in the ‘belly’ of the bell curve, those investments are priced efficiently. However, when you go out to the extreme tails, the price understates the reward for the risk…as the theory goes.

Asymmetric Bets recognizes humans do a poor job of estimating tail events happening. Therefore, you take the barbell strategy and put it on steroids. You keep most your money in the most safe allocation possible, and put a small amount of money in the absolutely most degenerate investment possible. Overtime, enough of those moonshot investments will land to be a net positive on your portfolio.

For example, you could have most of your money in savings accounts, and then take a small amount of money and buy WAY out the money call options. (Need a refresher on call options? Review how buying call options works.)

[Example - If the market is saying there is a 1% chance of the option paying off for $10, it will price a call option ~$0.10. (1% x $10 = $0.10).

However, if the probability is really 2% and the payoff is $50, the price should be $1. If you get 100 chances in a year to buy the call option at $0.10, you will pay $10. Therefore, 2 times out of the 100 you would expect a payout of $50. So for your $10 investment you make a $100 (payout of $50 two times). That is a 10x on your investment. ]

If you had a $100 portfolio at the beginning of the year and 90% of it was in cash while 10% of it you purchased call options like above. At the end of the year you would have $190 in the portfolio. Your entire portfolio had a 90% return. However, your entire downside is a 10% loss. (ie-the most you can lose is the 10% allocation to risky assets.)

[‘Tism Note - You can use a conservative portfolio and options to set up a portfolio for nearly any level of risk using options.

A lower volatility strategy could be to buy bull call spreads. Let’s say you have $100 and can invest in 1-year CDs at 3%. You could:

Take $97 and buy a 1-yr CD with it, in a year that will grow to $100 again in a year

Take the $3s and buy an at-the-money call & sell an out-of-the-money call, such that the premium you pay for the 2 options is a net $3

Let’s say ATM call is $5 and a 10% OTM call is $2

Your payout on the total position is $100-$110 or (0-10%).

Or you can:

Take $95 and buy a 1-yr CD, in a year it will grow to $98

Take the $5 and buy an ATM call

Your payout is $98-infinity or (-2% to infinity%)

Both set-ups use the same securities to get different payouts. (note this is how insurance companies manage assets for indexed products like Indexed Universal Life (IUL) and Indexed Annuities (IA).]

Hedging Vs. Diversifying

So far we have largely discussed some different ways to diversify. Diversifying is very different than hedging. When you diversify, you buy assets that don’t move exactly together.

If asset A goes up $1 and asset B goes up $0.50, then buying A & B in a portfolio will ‘diversify’.

The level of diversification is usually calculated with the correlation between assets. Correlation is a measure that goes from -1 to 1. If 2 assets move:

Exactly the same, they have a correlation of 1.

Asset A goes up 1% then asset B goes up 1%

Randomly between eachother, they have a correlation of 0. This means the assets are completely independant

Asset A goes up 1%, then asset B does something random between going from negative to positive infinity percent

Exactly the opposite, they have a correlation of -1

Asset A goes up 1%, then asset B goes down 1%

Diversifying means the assets have a correlation <1. The closer to 0 correlation, the better the asset is for diversifying.

This is based on the concept of risk-adjusted returns, where the ‘risk’ is measured by volatility. By having assets not 100% correlated, you get less volatility for the return.

[‘Tism Note - there is a lot of arguments to be made against the typical risk-adjusted return frameworks like sharpe ratio, but its good enough for here]

Hedging is when you buy an asset that explicitly moves in the opposite direction as your portfolio. A good example of a hedge is buying a stock and then buying a put on that stock. If the stock goes down, the put value goes up to offset the decrease in the stock.

Which seques into the strategy of…

Protective Puts

Protective puts is when you buy a put on an underlying stock you own. You pay a premium and the value of the put goes up if the price of the stock goes down. (Read a refresher on put buying here)

Protective puts are a fairly lower cost way of hedging a position.

In the screen shot above, if you had 100 shares of the SPY, you would have a $39,227 position in the ETF. You could buy one $392 put on SPY for $969 (nice) that expires in a month. For every dollar below $392 the SPY has fallen on 8/19 close, the option will pay out $100.

If the SPY ends at $382, your stock position is $38,200 and you have the right to sell 100 shares of SPY for $392 a share from your put, so your put will pay off $1,000. ($39,200 - $38,200). Therefore, your net position is back to $39,200.

$969 / $39,277 = ~2.5%. So you are paying a 2.5% monthly cost currently for 1 month of portfolio protection. As you can imagine, this quickly adds up over time. In a bull market, it usually costs 1% a month to put a trailing protective hedge on.

[‘Tism Note - The high cost of protective puts means most people don’t 100% hedge. If you have 500 shares of SPY, maybe you only buy 2 puts. It gives you some hedging, but at a lower cost.]

Inverse ETFs

Another option out there are inverse ETFs. These are supposed to track the inverse of an index. This is similar to shorting the index with the benefit of you can only lose 100%. (When you short, you can lose infinite percent).

Inverse ETF tend to have fairly high expenses ($RWM has nearly a 1% expense ratio). But over shorter periods of time can serve as a good hedge to your holdings.

As you can see above, if you bought & held the inverse Russell ($RWM) you would be up ~11.5% over the last year, while the broaders Russell Index ($IWM) is down ~16.5% over the same period. Even accounting for the 1% fee, you can see that the short Russell ETF isn’t a perfect hedge and there is some performance slippage.

[Note - Yes, we realize RWM is a better ticker for the Russell with IWM being a better ticker for the Inverse RWM…We didn’t make the tickers….And it triggers us everytime]

We tend to invest in smaller cap and higher-beta names that are closer to $IWM than $SPY so we do use the inverse ETF on occassions as a quick & easy hedge of the beta in our holdings.

Liquidity

Risk management isn’t just for the volatility of the asset or the expected returns of the asset - it also has to do with managing liquidity.

Arguably, liquidity is the most important part of risk management. If you have liquidity you can weather any storm. The opposite isn’t true….If you have lots of assets but they are all locked up in illiquid investments, you can still wind up busted.

Lets say you had a guaranteed return of 9% on an asset, great. But if you need to lock it down for 30 yrs would you put every bit of your savings into it? What if you didn’t have enough cash flow today to cover your expenses?

This is one of the main reasons I wouldn’t recommend paying off your mortgage until you are fully financially free. If you have $10 million in the bank and want to pay off a mortgage, that is fine. If you have $200k in total savings & investments, and you use it to pay off your mortgage, that is a different story.

Yes, you dropped your monthly expenses, but if a $30k expense pops up tomorrow you are ill-prepared for it. Now what if that $30k expense pops up when the housing market is down and banks are being stingy? You may not be able to get any cash out of your home and forced selling into a poor market.

Leverage

The opposite side of the coin is the amount of leverage you have. Think of leverage as your borrowing. Each loan you take out gives you cash today, but burdens you with a future expense stream.

The more leverage you have, the higher your % return may be, but it comes with a higher risk, especially of a spectacular blow up. If you have been paying any attention to crypto, you have seen investors and hedge funds blow up due to being over-leveraged.

Leverage works like this:

You deposit $100 and use it as collateral to take out a loan for $500

You owe $25 in interest payments on your $500 loan (5% rate)

You invest the $500 and let’s say it goes to $625 (a 25% return for the year)

You pay off the loan & interest and get your original deposit back.

Your net return was $100, from $625 -$25 - $500, and the total cash you deposited for collateral was $100. So even though your investment went up 25% (from $500 to $625), since you took out a loan and leverage, your actual net return on your money is 100% (from the $100 you made on $100 of deposit)

Works great when it works. But lets say that the loan comes with a covenant (rule) that you need to keep a $100 balance between the loan amount and the assets you purchased. (ie- your investment drops to $450 from $500, that means you have $100 deposit + $450 balance - $500 loan = $50 < $100, so you would need to add $50 to the collateral. A 10% decrease in the asset leads to a 50% increase in the money you need for collateral).

All the debt you have is leverage on your holistic personal finances.

Conclusion - Risk Management 101

These are some basic risk management concepts you should be familiar with. Once these make intuitive sense, you can start building a framework for you to follow.

When looking at your portfolio you need to consider how you diversify by choosing assets with different risks and liquidity, consider hedging, and keep an eye on your overall amount of leverage.

In actuality, most people don’t set up a true ladder or barbell portfolio. However it is a useful way to bucket and think about various risks.

One last concept we really like to deploy is selling calls on securities you own. When you sell a call you are partially offsetting your risk by the premium amount. If the market is flat or down, you get a little protection without giving up all the upside. It is a minor hedge.