Option Basics Part 5: Moneyness, The Greeks, and Put-Call Parity

Building Intuition around options

We have talked about options a lot. Once you understand how they work, the next step is to learn about how to talk and think about options. This post is going to introduce and go a little deeper into some concepts we have previously mentioned to help you further internalize how options work.

We will go over 3 important aspects of options:

Moneyness

The Greeks

Put-Call Parity

1) Moneyness

An important concept with options is how “in-the-money” the option is. In-the-moneyness is a measure of the current exercisable value of the option or intrinsic value. In layman’s term, if the option matured was right now, would there be any value in it.

For a call option, the call option value is higher as the stock price increases, therefore the option is:

In-the-money (ITM) when the stock price > strike price

At-the-money (ATM) when the stock price = strike price

Out-the-money (OTM) when the stock price < strike price

For a put option it is the opposite. The put option value is higher as the stock price decreases, therefore the option is:

In-the-money (ITM) when the stock price < strike price

At-the-money (ATM) when the stock price = strike price

Out-the-money (OTM) when the stock price > strike price

So the more in-the-money an option is, the higher the value. The level of moneyness will also impact how sensitive an option is to changes in variables. Or said another way, the value of the Greeks changes as the moneyness of the option changes.

2) The Greeks

Depending on your life you may think of frats / sororities, an ancient culture, that delicious restaurant, or a big loud family. The Greeks we are dealing with pertain to options.

There are 5 core Greeks: Delta, Gamma, Theta, Rho, & Vega. So what are they and why should you care?

Previously we covered the 4 basic option positions:

The Greeks are metrics that are used extensively in hedging programs by big institutions. They measure the sensitivity of your option price to changes in the underlying market.

The real important aspect of the Greeks as a starting retail investor is to understand how option prices move from each item. (Also, then you can casually drop things like ‘Theta decay’ and ‘Vega reversion’ and seem like a gigabrain).

What Are Option Greeks?

In short, each Greek is measuring how much the price of an option changes as the market moves. You can think of them as the sensitivity the option price has to each variable.

For example, if the variable moves up 1 unit then:

If the option price moves up 1 unit, the resulting Greek would be 1 = 1/1.

If the option price moves up 0.5 units, the resulting Greek would be 0.5

If the option price moves down 0.5 units, the resulting Greek would be -0.5

Pretty easy right?

The Greeks are derived from the commonly used option pricing formula Black-Scholes.

Value of an Option

The 6+ previous posts we did on options all ignored any option value between purchase and maturity. However, standard options are traded every day just like any other security. The Greeks help you understand how the price of your option will change as the underlying parameters change. There are times it makes sense to close out an option position before expiration.

The Greeks help you gain an intuition about how the price of your option may react to market changes. This will help you to determine if you should roll your option or when you may want to trade out of it.

What is the Black-Scholes Formula?

Black-Scholes was one of the first formulas developed to calculate the intrinsic value of options in the market back in the 1970s. Black-Scholes has been expanded on over the years to include items left off the original formula (like dividends) and to refine some of the simplifying assumptions (like Normal Distribution of returns).

However, you can find most of the Greeks already calculated for you on many trading platforms. Honestly, you can never calculate Black-Scholes or Greeks manually in your career.

You only need to see the formula to know the variables in it that impact options intrinsic value. The Black-Scholes Formulas for a call option and put option are:

The Greeks of Options

So what are the variables in the formula:

Current Stock Price (Delta & Gamma)

Risk-free interest (Rho)

Time (Theta)

Volatility (Vega)

The Greek letters chosen correspond with the first letter of the variable for Rho, Theta, and Vega making it a little easier to remember.

We don’t think you need the actual formulas of the Greeks (you can go to the Wikipedia page of the Greeks if you really want to see them). Basically, they are all calculated as partial derivatives from Black-Scholes.

[‘Tism Note - ‘partial derivative’ here is the calculus method of measuring rate of change. So for options, a ‘partial derivative’ means measuring the rate of change of the price of the option for a unit change in only one variable, all else equal. If you look at the formula for Call and Put price above, you have an equation with S, K, T, r, sigma.

A partial derivative calculates the change in option price for the change in stock price (S) or the change in option price for the change in time (T), or the change in option price for a change in any 1 of the variables.

A partial derivative is different than the term ‘derivative’ that is used when talking about options in general. Options are derivatives because you don’t own the actual underlying asset. You own a contract that is an agreement for that asset at a pre-determined price by a pre-determined date. In calculus, taking a derivative of a formula is seeing the rate of change (ie the derivative of X^2 => 2X and the derivative of 2X => 2, etc…not to bring you back to math class in school)

So to make it sufficiently confusing, the Greeks are partial derivatives on derivative securities]

Delta of an Option

Delta is the rate of change of the option price for a 1 unit change in the underlying stock price.

But an option price doesn’t change 1:1 with the underlying stock. Remember, if your option expires out of the money (OTM), you get $0. It doesn’t matter if you are $0.01 out of the money or $1,000 OTM. Therefore, intuitively if your option is very far out of the money, a small change in the stock price has a small impact as you are still very unlikely to make money.

Additionally, if your option expires in the money, your payoff is the difference in the stock price and the strike price. A $1 difference in the stock price leads to an exact $1 difference in your payoff. Therefore, if you are very far in the money (ITM), each change in the underlying stock price leads to a near 1:1 impact on your option.

The result is an shape of your Delta like the one below:

The more OTM you are, the closer to 0 the delta is (indicating no impact to changes in the stock) and the more ITM you are, the closer to 1 the delta is (indicating each change in the stock leads to a near equal change in the option).

If you are at the money (ATM), it means a small change impacts if you are ITM or OTM and the delta is 0.5.

The shape of the delta curve is not linear as the sensitivity to delta changes, which is captured by our second Greek, Gamma.

Gamma of an Option

Gamma is the rate of change of an option’s delta.

As stated above in the delta section, an option’s price will change more when it is ITM vs OTM, for a 1 unit change in the underlying. If a deep ITM option has a delta of 1, an ATM option has a delta of 0.5 and a deep OTM option has a delta close to 0, as the underlying stock continues to be more ITM, the sensitivity of the option price increases towards 1.

Gamma tells you how much your delta changes.

When an option is ATM, gamma is maximized. This makes sense if you think it through. Consider a call option with a $10 strike and 1 day to maturity:

If the stock price is $1 it is deeply OTM and likely to expire worthless since you only have 1 day to get over $10. Deeply OTM options have deltas close to 0. If the price of the stock increases to $2, the option still expires worthless. Therefore, the change in delta will be from 0ish to 0ish meaning the gamma is close to 0

Conversely, if the stock price is $20 it is deeply ITM and a $1 change in the underlying stock will result in nearly a $1 change in the price of the option. (Since the strike is $10, at a $20 stock price the option pays out $10 and at a $21 stock price it pays out $11.) Since the option price changes ~$1 for a $1 change in the stock, the delta as the stock goes from $19 to $20 to $21 goes from 1ish to 1ish. This again means the gamma is close to 0 (ie-delta’s value doesn’t change as it goes from 1ish to 1ish)

If the stock is at $10 and ATM, a $1 stock price decrease means the option expires OTM and worthless and a $1 stock price increase means the option expires ITM and worth $1. Therefore, the price of the option will change drastically if the stock goes from $9 to $10 to $11. The change in delta will be highest, meaning gamma is the highest for ATM options.

[‘Tism Note - The delta of an option ATM the instant before maturity is 0.5 according to BS model. Therefore, an ATM option has a delta ~0.5 meaning a $0.02 move in the stock price results in a $0.01 move in the option price FROM delta (the actual option price is change more due to the other Greeks moving)]

Theta of an Option

Theta is the rate of change in the option price from the passage of time.

In general, the longer you have till option maturity, the higher the Theta. Intuitively, you would pay more for an option that expires in 1 year than one that expires in 1 day as you have more time for the underlying stock to move and finish ITM.

Theta Decay, Theta Burn, and Time Decay are all terms that capture this decrease in the price of an option as it approaches expiration. Theta Decay is a bad guy for the option buyer, but a good guy for the option seller.

This is why Theta is our favorite Greek and we like selling options.

If nothing changes, each day that passes is a transfer of value to the option seller as the price of the option decreases due to less time.

The only thing for certain in life is that time waits for nothing.

Vega Of An Option

Vega measures the sensitivity of an option’s price to the underlying volatility of the stock price.

Intuitively, the more volatile a stock price, the more likely it is to make large changes and the more likely the option expires ITM. Therefore, the more volatile the underlying stock is, the higher the Vega and the higher the option price is (ie- the more you would pay to own it).

The important aspect of Vega is that it will jump up if the underlying stock has a big move.

For example, if news comes out and the stock price changes 20% on the day, the Vega of the option will skyrocket which will make the option prices all go way up. If the stock price then settles down at the new price level and only changes small 0.1% moves for a while, the Vega will trend back down.

As an option investor, selling options on stocks after big moves tends to capture the best premiums.

Rho of an option

Rho is the least exciting Greek and included for completeness. It measures the change in the option for changes in the ‘risk-free’ interest rate.

Higher risk-free rates tend to correspond with higher option prices. But the impact of Rho is dwarfed by the other Greeks. Just be aware it is there and what it is, but there isn’t much value in describing it more.

Greeks in Hedging

Why are the Greeks useful in hedging? At their core, the Greeks measure the sensitivity of an underlying stock or portfolio to the change in the variable. In theory, if you match each Greek in your hedge portfolio to the target, you are completely neutral to any movements, aka perfectly hedged.

If you reach a perfect hedge, each 1 unit move in the target portfolio is matched with a 1 unit move in the hedge. In practice this is impossible due to the 2nd order and cross-correlations so a hedge portfolio needs rebalancing over time. However, hedging across the 5 main Greeks shown and using monthly rebalance can typically get you over 90% hedged. (Note - Rho tends to be fairly immaterial for most purposes).

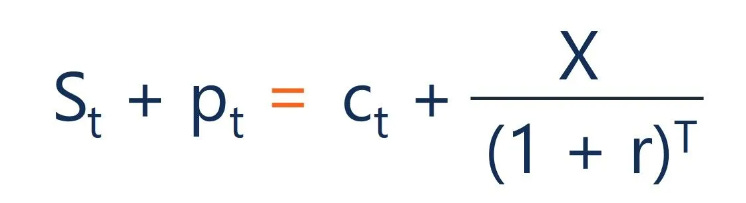

3) Put-Call Parity

The put-call parity is a concept that sets the relationship between puts, calls, and the underlying security. If the relationship doesn’t hold, then there is an arbitrage opportunity.

The put-call parity formula is interesting to be aware of, and if you want to deep dive into it, you can read more here (where the above formula is copied from).

The basics is that you can create ‘synthetic’ calls and puts by buying and selling:

The underlying stock

A call/put with the same strike and maturity

Cash at the risk-free rate

In theory with a frictionless transaction, if the relationship doesn’t hold you could buy or short the option and create a synthetic version that has the exact same payoff. Then you get a risk-free profit.

Interesting. Good to be aware of. But requires sophistication that is likely outside the scope of a retail investor. Therefore, we won’t spend any more time on it.

Conclusion: Option Basics of Moneyness, Greeks, and Put-Call Parity

There is the next step in your option education.

If you can develop intuition around these concepts, you are able to talk options with most people and it will help you as you look to invest.

If you want to read more about strategies, we have written about:

Using Options To Increase Returns & Decrease Volatility

Good luck with your trading Anon.

Perfectly well described 👏