Introduction to Bonds

What To Know If you are considering locking in some of the new higher yields

Bonds are getting a lot of attention. Some of the reasons are good. Others, not so much. If you are like most people, you just put some token allocation (5%) of your 401k into whatever bond ETF is offered and don’t think much about it (foreshadowing - a future post will tell you why bond ETFs are largely trash bandicoot).

Or maybe you have some vague sense that bonds are ‘safer’ so your target-date fund allocates more to bonds over time.

We spent the first chunk of our careers as a strategist in a fixed income asset management firm, and 2 things surprised us when it came to bonds (also known as fixed income):

They are infinitely more complex and nuanced than stocks

The people playing in the bond markets are heavily made up of the ‘smart money’

So what are bonds, how does it all work, and why should you care?

Why You Have Heard About Bonds A Lot Recently

Ignoring the technical details for a moment, bonds are supposed to be a ‘safer’ asset than equities. At its simplest, you buy a 5 year bond with 4% coupon for $100 Par value and you get $4 a year for 5 years and your $100 back at maturity, assuming the firm doesn’t go bankrupt. This should make bond returns fairly stable, in theory.

Additionally, in a bankruptcy, bond holders are near the top of the payout ladder and equity holders last. This means, in theory, bond holders would get the full value of their bonds before equities holders are entitled to anything.

In short, bonds are supposed to be more stable / less volatile as they will ultimately return the yield at purchase if the company doesn’t go bankrupt. And even if the company goes bankrupt, you tend to get something back while equity goes to zero.

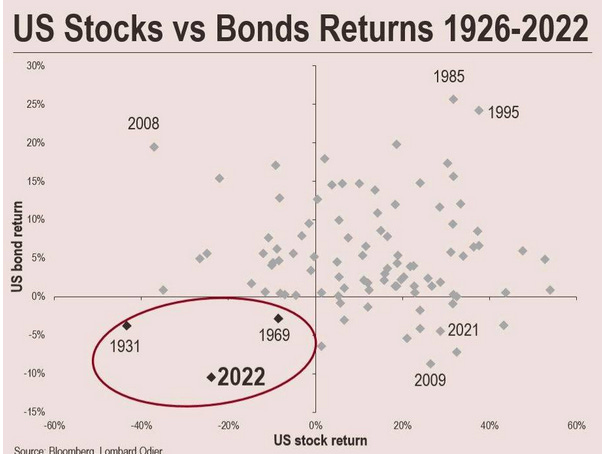

In 2022 however, bonds were nearly as volatile as equities and finished the year down double digits which almost never happens.

Just to really drive the point home….