Consumption Smoothing

What is it and is it Right for you?

Meet Brenden (Not real name). He is a friend of mine.

Brenden has a good job, makes good money, and lives a very froogal lifestyle. He is the guy who goes out, will get the $1 beer, then only drinks water once happy hour ends (there is a huge mark-up on bar drinks). He wants bills split. And is guaranteed to ping you a Venmo request for your half of any ride (Ha - F’er doesn’t have pay apps on his phone though).

Somehow he got married (at a courthouse followed by a small reception at a public park). And he has 1 kid (anymore is crazy - it cost $350k to raise a child!!! (It doesn’t-not even close)).

Vacations? You mean staycation because travel adds up.

Brenden enjoys his paid off house that he got from his grandparents. Sure it still has pink tile in the bathroom since it was built in the 70s, but things mostly work.

Brenden’s wife still works full-time. She has expressed how she wishes she had more time with her kid, but ‘2 incomes are better than 1’.

And of course, the cherry on top, his wife and him share the old Toyota Camry. Brenden drops his wife off at work and picks her up after. 2 cars = 2 insurance payments and 2 property taxes.

I would say Brenden got 1 too many budgetpoor courses, but no way he dropped $5,000 on anything…ever.

But Brenden does have a well above average net worth. To put some numbers around it, lets say he has $2 mm and is 40 years old. If he does nothing else and you assume markets earn 7% a year over the next 25 years, this will grow to like $8 million - even without anymore saving or investing.

From a numbers perspective, he is doing well.

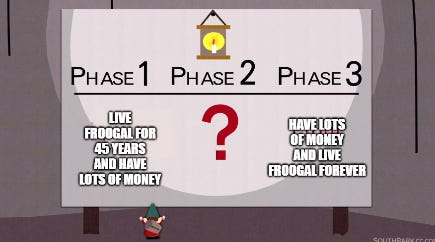

And if you talk to him, he has a plan. The plan looks something like this:

Even if later in life he breaks the spell of Davey Ramsey and starts to spend, and if you know Brenden you know that doesn’t look likely, how much joy do you get spending in your 60s vs 20s?

Is there a better way to approach spending and saving?

Some Caveats Before We Start

Before we start talking about consumption smoothing, lets address some important points here.

First, Brenden is atypical in the USA today. A lot of people spend way more than they make. They are forever trying to ‘keep up with the Jones’ and live in debt for most of their adult lives.

This is the other end of the spectrum and arguably just as bad.

Nothing in this post is a recommendation to forever be in debt.

Second, this requires some self-discipline and honesty. You can’t be in a career where you top out at $50k a year but spend like at some point you will hit $200k. As time goes on, you need to stick to your plan and really start saving and investing. Since you miss out on years of compounding, you need to put more of your own money in later to offset the growth you missed out on early.

Lastly, you need to think long-term and actually have a plan that you track.

But if done well, this may be the optimal way to spend in your adult life. Let’s break it down.